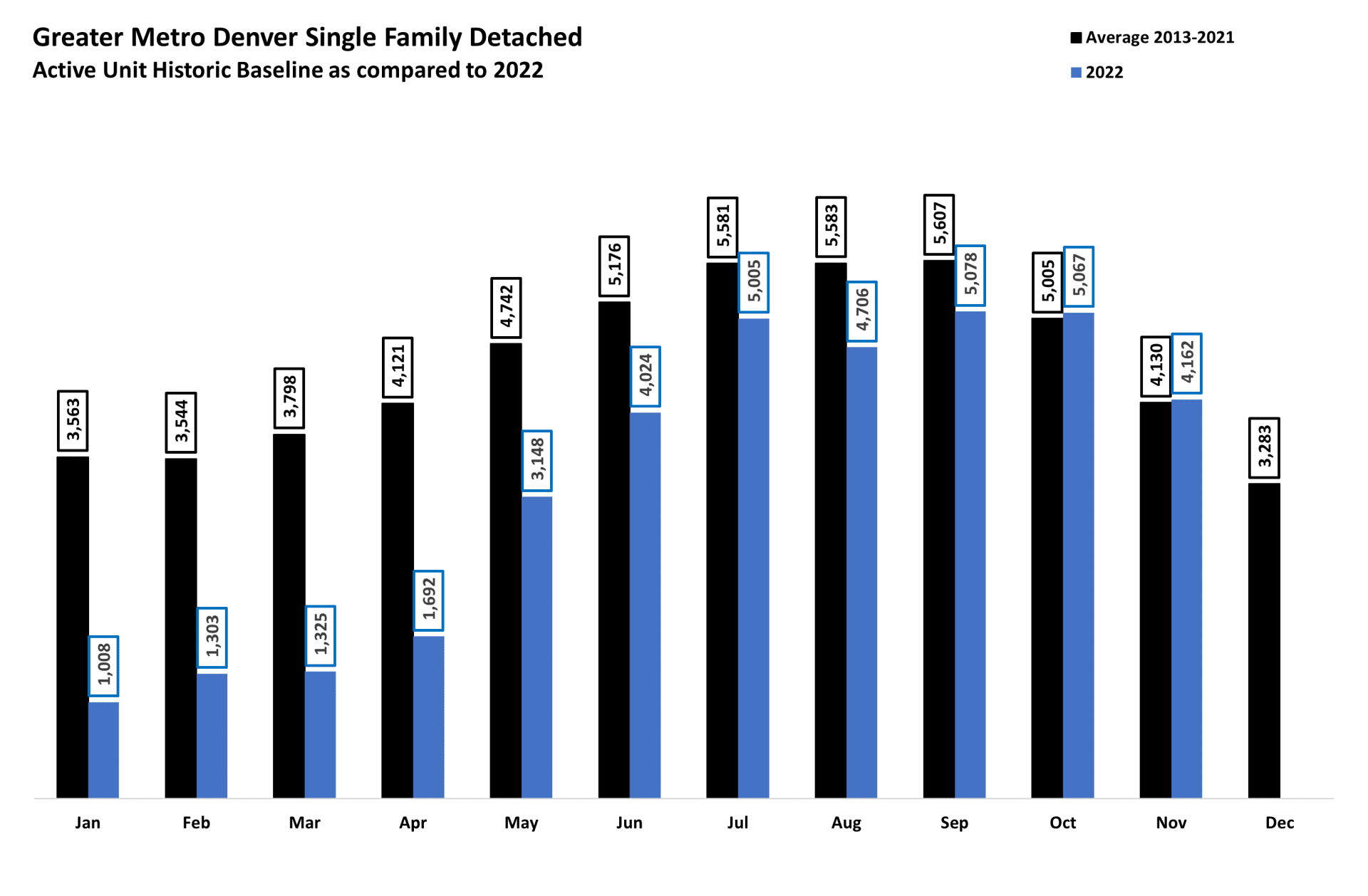

Fewer new listings, more expired and withdrawn driving inventory down.

The media continues to report that inventory is way up, and while it's true that inventory is way up from 2021 when we look back over the last 9 years we are about where we should be for inventory levels heading into the holidays. It's back to 2013-2019 in terms of market activity, to get a good baseline we truly need to remove the pandemic years from the equation so taking out 2020, 2021 and the beginning of 2022 to get a grasp on what we are dealing with now. Here is a snapshot of historical inventory levels for detached single family going back to 2013. Inventory is coming on at a slower rate and expired and withdrawn transactions are up as we get closer to Christmas.

With the purge of listings from our market, months of inventory went down this last week by -11.8% to 1.8 months of inventory. Our average daily active count fell by -4.8% to 5,730 listings available for sale heading into last weekend in the 7 metro counties. Pending transactions continued to pick up week over week with 724 units going under contract, which was up by 7.3% over the last week but still down from 2021 by -22.2%. We will continue to see listings pull from the market later into December leaving buyers with fewer choices, but they have great negotiating power right now as price reductions on average last week was 8% off of the original price. Buyers will likely continue to have leverage in this market until next spring giving them a small golden window to exercise their negotiating power. Sellers are offering incentives such as rate buy downs and closing costs to sweeten the deal and get it done before the end of the year.